The romanticized image of a startup usually involves a garage, a brilliant idea, and a sudden influx of venture capital. The reality, however, is often found in the ledger. Statistics consistently show that the majority of new businesses don’t fail because their product was bad or their market didn’t exist; they fail because they ran out of cash.

In the UK’s competitive landscape, accounting for startups is frequently treated as a “Phase 2” activity, something to be handled once the business is “real.” This is a fundamental error. Robust financial control is not just about staying on the right side of HMRC; it is about survival. It is the difference between making a strategic pivot and being forced to close your doors.

This guide provides a stage-by-stage financial checklist designed to take you from your initial HMRC registration to a scale-up ready for investment.

Why Financial Planning Is Critical for Startups

Many founders operate under the “build it and they will come” philosophy, assuming that as long as sales are growing, the finances will take care of themselves. This ignores the silent killers of new enterprises.

The Hidden Risks of Poor Financial Management

- Cash Flow Mismanagement: You can be profitable on paper but still go bankrupt because your cash is tied up in unpaid invoices while your bills are due now.

- HMRC Penalties: The UK tax system is efficient but unforgiving. Missing a VAT or Corporation Tax deadline can result in automated penalties that drain your early-stage capital.

- Missed Growth Opportunities: Without clean data, you won’t know when you can actually afford to hire that vital lead developer or move into a larger office.

Common Misconceptions Founders Have

One of the biggest hurdles in accounting for startups is the “Profit = Cash” myth. Profit is an accounting metric; cash is what pays the rent. Furthermore, many founders believe spreadsheets are sufficient for the first year. While Excel is powerful, it lacks the automated bank feeds and tax compliance features that modern cloud software provides, leading to manual errors that can take weeks to untangle later.

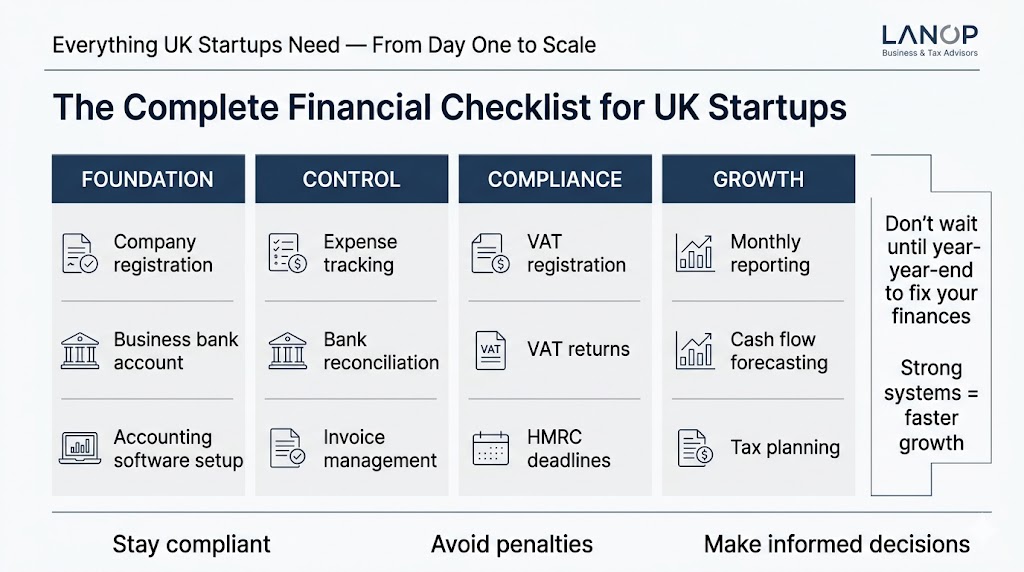

The Complete Financial Checklist: From Setup to Growth

Stage 1: Before You Launch (The Foundation)

Before the first sale is made, you must build a legal and financial shell that protects you and your assets.

1. Choose Your Business Structure

In the UK, you typically choose between being a Sole Trader or a Limited Company.

- Sole Trader: Easier to set up but offers no “limited liability,” meaning you are personally responsible for business debts.

- Limited Company: More tax-efficient at higher profit levels and protects your personal assets, but comes with significantly more administrative and accounting requirements.

2. Register with HMRC and Companies House

If you go the Limited route, you must register with Companies House. Regardless of structure, you must notify HMRC that you are trading to ensure you are set up for Self Assessment or Corporation Tax.

3. Open a Business Bank Account

Never mix personal and business funds. Even as a sole trader, having a dedicated account makes your accounting for startups ten times simpler.

4. Choose Your Accounting Method

- Cash Basis: You record income and expenses when money actually changes hands. (Simpler, usually for smaller businesses).

- Accrual Basis: You record income and expenses when they are invoiced or incurred. (Standard for Limited companies and essential for understanding true performance).

5. Select Accounting Software

Avoid the “shoebox of receipts” trap. Platforms like Xero, QuickBooks, or FreeAgent are the industry standards in the UK. They connect directly to your bank account and automate much of the heavy lifting.

Stage 2: The First 30–90 Days (Building Systems)

The goal here is to stop “guessing” how much money you have and start “knowing.”

- Track Every Single Expense: From a £3 coffee with a client to a £2,000 software subscription. Use tools like Dext or Hubdoc to snap photos of receipts instantly.

- Set Up a Weekly Finance Routine: Spend 30 minutes every Friday categorizing transactions. If you leave it for a month, you will forget what that “AMZN MKTP” charge was for.

- Calculate Your Burn Rate: This is the amount of money you are spending each month.

- Know Your Runway: If you have £50,000 in the bank and your burn rate is £5,000 a month, you have a 10-month runway.

$$Runway\ (Months) = \frac{Total\ Cash}{Monthly\ Burn\ Rate}$$

Stage 3: The First Year (The Stability Phase)

This stage is about navigating the “First Year Hurdles” specifically HMRC deadlines and VAT.

1. Stay Compliant

- VAT Returns: If your taxable turnover exceeds £90,000 in a rolling 12-month period, you must register for VAT. Many startups register early to reclaim VAT on their setup costs.

- Corporation Tax: You must pay this within 9 months and 1 day after your accounting period ends.

- Confirmation Statement: An annual “check-in” with Companies House to confirm your directors and shareholding.

2. Monthly Financial Health Check

Reconcile your bank accounts at the end of every month. Review your Profit and Loss (P&L) statement. Are your margins what you expected? If your cost of goods is creeping up, you need to know now, not at the end of the tax year.

Stage 4: Growth & Scaling

When you move from “surviving” to “thriving,” your financial needs become more complex.

- Move Beyond Basic Bookkeeping: Start looking at Cash Flow Forecasting. Use software that projects your bank balance 3–6 months ahead based on your current spending patterns and expected sales.

- Automate Everything: If you’re hiring, integrate your payroll software (like BrightPay or Gusto) with your accounting platform.

- Prepare for Funding: If you plan to seek VC or Angel investment, your “books” need to be pristine. Investors will perform due diligence; if your records are messy, it signals a lack of professional control and can kill a deal.

Your Operational Checklist: Weekly, Monthly, Quarterly

To make accounting for startups manageable, break it down into small, recurring tasks.

Weekly

- Categorize all bank transactions in your software.

- Snap/Upload all physical and digital receipts.

- Review “Aged Debtors” (who owes you money?) and send polite reminders.

Monthly

- Perform a full bank reconciliation.

- Review P&L vs. Budget. Where did you overspend?

- Set aside tax funds. A common mistake is spending the money you actually owe to HMRC. Move 20-25% of your profit into a separate savings account immediately.

Quarterly

- File VAT returns (if registered).

- Review your “Runway.” Do you need to raise more capital or cut costs?

- Meet with your tax advisor to discuss tax-planning opportunities (like R&D Tax Credits).

Key Financial Decisions Every Startup Must Make

Should You DIY or Hire an Accountant?

DIY Works If:

- You are a pre-revenue or very low-volume sole trader.

- You have a genuine interest in learning the basics of UK tax law.

Hire an Accountant When:

- You incorporate as a Limited Company. (The filing requirements are too complex for most non-professionals).

- You register for VAT.

- You start hiring employees.

- Your time is better spent on product development or sales than on reconciliation.

Choosing the Right Software

- Xero: Best for scalability and has the most “Add-ons” for inventory or project management.

- QuickBooks: Very user-friendly for non-accountants and often slightly cheaper for entry-level plans.

- FreeAgent: Often free if you have a business account with banks like NatWest or Mettle; excellent for contractors.

Common Financial Mistakes UK Startups Make

Even the smartest founders fall into these traps. Here is how to avoid them:

- Mixing Personal and Business Finances: This creates a nightmare for your accountant and can jeopardize your “limited liability” status. If you pay for a business dinner on your personal card, record it as an “expense claim,” don’t just leave it in the personal account.

- Ignoring VAT Thresholds: HMRC checks turnover on a rolling 12-month basis, not a calendar year. If you go over £90,000 and don’t register, you will be liable for the VAT you should have collected from your customers out of your own pocket.

- Missing R&D Tax Credits: The UK government offers generous tax breaks for companies “innovating” in science or technology. Many startups don’t realize that “developing a unique software platform” often qualifies for these credits, which can be worth thousands in cash rebates.

Essential Financial Metrics to Track

In accounting for startups, these four metrics are your “dashboard”:

| Metric | Definition | Why It Matters |

| CAC | Cost per Acquisition | How much does it cost to get one new customer? |

| LTV | Lifetime Value | How much revenue will one customer bring over time? |

| Gross Margin | Sales minus direct costs | Tells you if your core business model is actually profitable. |

| Burn Rate | Monthly negative cash flow | Tells you how fast you are “bleeding” cash before reaching break-even. |

Real Startup Scenarios (The Reality Check)

I just crossed the £90,000 turnover mark. What now?

You have 30 days to register for VAT with HMRC. You should also consider whether the Flat Rate Scheme would save you money or if the Standard Scheme is better (especially if you have high business expenses).

I missed my Corporation Tax deadline. Help!

Don’t wait. HMRC is more lenient if you approach them first. You may be able to set up a “Time to Pay” arrangement. The longer you wait, the higher the interest and penalties climb.

I’m still using a spreadsheet. Is it too late to switch?

No. Most modern software allows you to import your CSV files from Excel. The sooner you move to a system with automated bank feeds, the sooner you eliminate human error.

When to Get Experts Help?

There comes a point where “doing the books” yourself becomes a liability. If you find yourself spending more than 5 hours a month on admin, or if you feel a sense of dread every time an HMRC letter arrives, you have outgrown DIY.

Lanop Business and Tax Advisors specializes in taking startups from that initial “garage” phase through to robust, scale-up success. We provide the structural clarity you need so you can focus on your product, not your receipts. We don’t just “file your taxes”.we act as your strategic partner to ensure your runway is long enough to reach your goals.

FAQS(Frequently Asked Questions)

What are the first financial steps when registering?

Register your company at Companies House and open a dedicated business bank account straight away never mix personal and business money. You must notify HMRC for Corporation Tax within 3 months of starting to trade or you’ll face penalties. Set up bookkeeping software like Xero or FreeAgent from day one so your records are clean from the start. Getting an accountant early, even part-time, pays for itself quickly.

When do I need to register for VAT?

VAT registration is compulsory once your taxable turnover exceeds £90,000 in any rolling 12-month period missing this triggers automatic penalties. Many startups register voluntarily before hitting that threshold to reclaim VAT on early purchases like equipment and software. The downside is you must charge VAT to customers, which can hurt competitiveness if you sell to consumers. All VAT-registered businesses must also use Making Tax Digital-compatible software for their returns.

What do I need when hiring my first employee?

Register as an employer with HMRC before your first payday.it takes up to 5 working days so don’t leave it late. You’ll need to run PAYE, deducting Income Tax and National Insurance from each employee’s pay and sending it to HMRC monthly. On top of that, you pay employer NICs at 13.8% on earnings above £9,100 per year, which is a real cost to factor into your hiring budget. You must also auto-enrol eligible employees into a workplace pension and contribute at least 3% of qualifying earnings.

What tax reliefs should UK startups know about?

SEIS and EIS are the UK’s flagship startup investment schemes.They give angel investors 50% and 30% tax relief respectively, making your startup far more attractive to raise from. R&D Tax Credits let you reclaim up to 33p per £1 spent on qualifying innovation work, which can be a significant cash injection for tech startups. Innovate UK offers non-dilutive grant funding worth monitoring if you’re working on anything cutting-edge. All of these require advance planning.SEIS and EIS in particular need HMRC advance assurance, which takes 4–8 weeks.

How do I manage cash flow in the early stages?

Know your burn rate and divide your cash balance by it to see how many months of runway you have aim to always have 6 months visible. Build a 13-week rolling cash forecast so you can spot problems early, not when it’s too late. Invoice promptly and chase payments actively, since many UK businesses stretch to 60–90 day payment terms despite 30 being standard. Always map out upcoming HMRC payments VAT, PAYE, and Corporation Tax are easy to forget and can hit all at once.

What financial controls do I need as we scale?

Move to monthly management accounts, a proper P&L, balance sheet, and cash flow statement so you’re running on real numbers, not gut feel. Set clear expense approval limits so not every purchase needs a founder’s sign-off, but overspending still has a check. Track 5–8 consistent KPIs like gross margin, runway, and customer acquisition cost every month without fail. If you’ve issued shares or options, use a cap table tool like Carta or SeedLegals to stay on top of dilution and vesting schedules accurately.

Final Thoughts

Build Financial Clarity from Day One

At Lanop Business and Tax Advisors, we believe that accounting for startups is not about looking back at what happened last year.it is about giving you the data to decide what happens next. Too many promising UK businesses fall apart not because of a bad idea, but because of avoidable financial missteps like a missed VAT deadline, a payroll error, or simply running out of runway. By setting up a simple, disciplined financial checklist from the very beginning, you lay the groundwork for a business that can grow with confidence.

At Lanop, we work alongside startups and growing businesses every step of the way from company registration and tax planning to payroll, R&D claims, and investor-ready reporting. If you would like to talk through your financial setup or need a customised plan for your startup, the Lanop team is ready to help. Control your numbers, or they will eventually control you.